How to Make the Most Money Selling Your Home

- 50 Cities With Cheap Rent and Good Jobs for New College Grads

- 10 Cities Where the Housing Crash Still Looms Largest

- The Surprising Reason You Should Live Near Your Parents

- Buying a Home Is a Perfectly Fine Decision. It's Just Not a Financial One

- 'How We Did It': 3 Millennial Homeowners Tell Their Stories

In theory, selling a home should be easy right now. Real estate has been rebounding for more than half a decade, and home prices are climbing at a healthy 6% annual clip. The improving economy is creating a slew of would-be buyers, and there's a dearth of homes for sale.

On paper, this has all the makings of a classic seller's market. And that should be good news for Americans who have been stuck in their homes since the mortgage crisis—or who are simply looking to move to more vibrant communities and economies, such as the towns on Money's 2017 Best Places to Live list.

Yet selling isn't so simple. Just ask Ligiah Villalobos. In 2006 the television and film writer bought a $499,000 condo in Culver City, Calif., four blocks away from Sony studios. At the time, she was head writer for the children's show Go, Diego! Go!

She assumed she'd live in the three-bedroom, two-bath condo for a few years and then use the profits to trade up to a larger, single-family home closer to the ocean. But those plans were dashed less than a year after moving in, thanks to the real estate crash.

Today things are looking up. Housing in the Los Angeles metro market has come roaring back. Her mortgage is back above water. And if she sold today, she'd make a profit on her condo. Yet Villalobos still feels trapped.

That's because while her home is gaining value, so are all the ones around her. If she sold, where could she afford to live? "In Los Angeles, it's very difficult to find a nice house for less than $750,000. I still have a goal of moving, but it's not going to happen for at least two or three years," Villalobos says.

This is becoming a common refrain throughout the nation. "For some time we have been hearing from sellers that are not listing because they are worried they won't be able to buy their next home in that market," says Redfin chief economist Nela Richardson.

Don't abandon hope. There are plenty of moves you can make to sell while improving the chances you'll be able to afford to move to your next Best Place.

Be willing to put in some elbow grease.

In this market, you need to make the most of the asset you currently own. And selling your home in "as is" condition could mean leaving money on the table, making it harder to afford your next place.

You're still likely to find a buyer—eventually—even if you don't put in any effort. But "you will likely lose some bidders, and you may give back some on price," says Ralph McLaughlin, chief economist at Trulia.

The key is not to go overboard. A large-scale remodel may be costly and may not recoup as much as a smaller, targeted project, studies show. In addition to general decluttering, where should you start?

Focus on curb appeal.

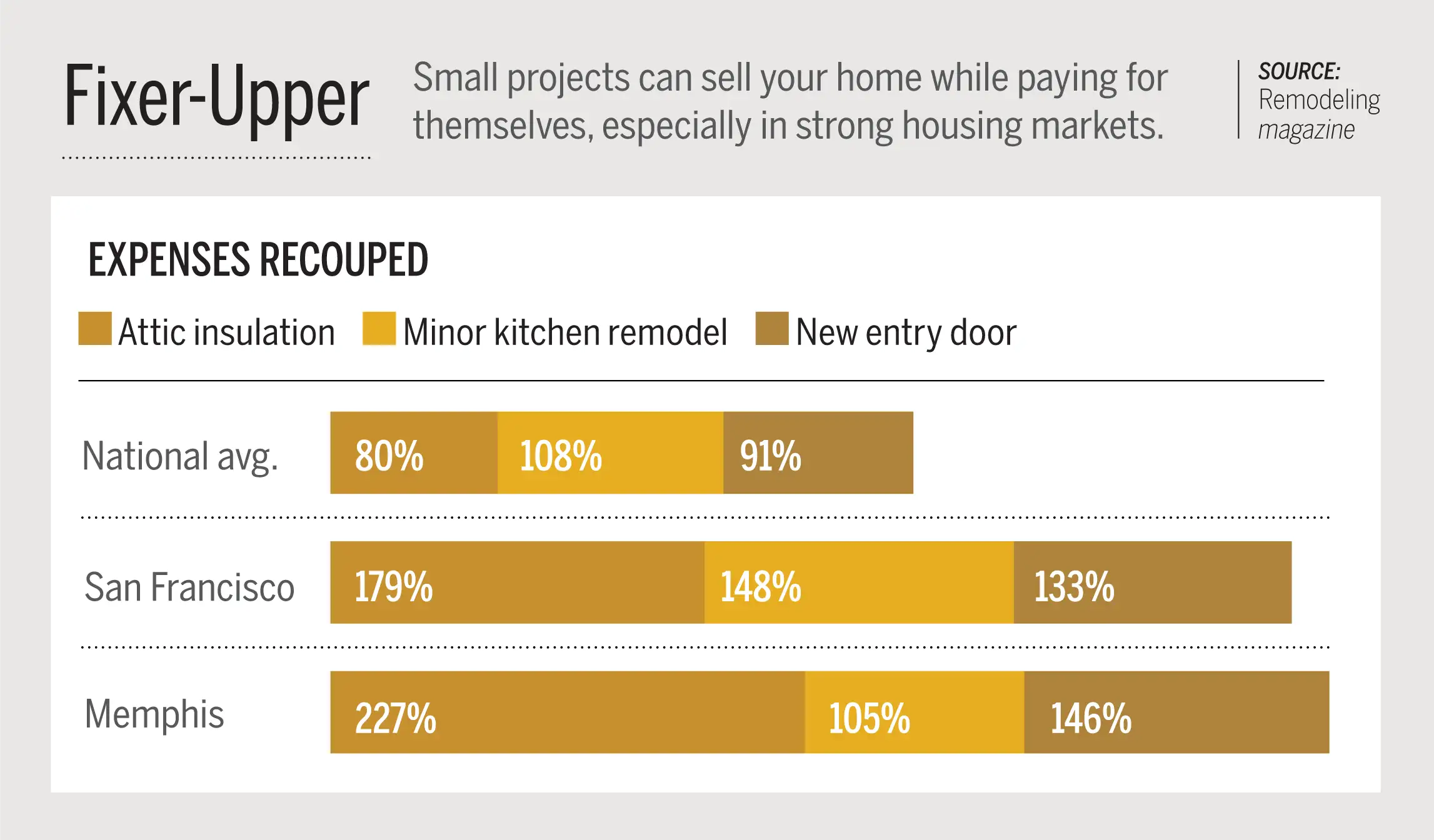

Among the small projects that retain the most value at resale, according to a survey by Remodeling magazine, are replacing your front entry door and garage door. Those are likely to be the first things a potential buyer will notice when pulling up to your house. Average cost: around $1,400 and $1,700, respectively.

Also, you'll recoup a far greater percentage of your costs on a minor kitchen remodel—think replacing old appliances, and refacing cabinets and surfaces—than on a gut renovation. Moreover, you're likely to spend around $20,000 on a minor touch-up, which is about a third of what a typical major kitchen remodel costs on average nationally.

Don't automatically jump on outlier bids.

It's natural to want to accept whichever bidder waves the highest price under your nose. But assuming that all of your home's bidders will be using a mortgage on the purchase, the offer price isn't the end of the story.

Their mortgage lenders will require an appraisal. If the appraisal comes in below the offer price, the lender will nix the deal unless the buyer coughs up more money to make up the difference—or you drop the price. If no one budges, you'll have to start all over again, setting your sale back.

To avoid this happening, work with a seasoned agent and listen to his or her guidance on which bid has the smoothest chance of sailing through the closing process.

Sell your property and lease it back immediately.

The old rule of thumb in real estate: location, location, location. The new rule: timing, timing, timing.

"Before we list we need to have a strategy for where the seller will go. Brokers are becoming relocation experts," says principal broker Sam Schneiderman of the Greater Boston Home Team.

You can buy yourself time by making your sale contingent on the buyer leasing the home back to you. Having another few months to stay can be just the breathing room you need to find and close on your next home.

This strategy works best in ultracompetitive seller's markets. "A buyer dealing with competition from other multiple bidders may be willing to do it, as a way to get your home," says Redfin's Richardson.

Be willing to make a pit stop in a rental.

Schneiderman says some of his clients are moving into rentals or temporary housing after a sale. That's to better position themselves as buyers who don't have to sell when they're making an offer on their next house. In the hot Boston market, you may lose out on four or more bids before landing your next home.

To make this less of a hassle, get a furnished rental and leave your possessions packed and in storage until you are ready to move into your permanent home.

Steer clear of bidding wars on your next home.

You can do this in a number of ways. First, a good agent should know everything that might appeal to a seller, like a fast close, a super-slow close, adopting their cat. Your bid should include any contingencies that specifically address stress points for the seller.

Also, consider a fixer-upper for your next home. Most buyers today want as close to a turnkey situation as possible. So if you shop for homes that need some work, you will likely face less competition.

And don't forget new construction. "Signing a contract with a builder avoids having to deal with bidding wars," says Sarah Staley, a housing spokesperson for realtor.com (Money has partnered with realtor.com for this year's Best Places to Live feature). This works if you can sit tight in your current home until your new home is ready.

Can't sell in a timely fashion? Become a landlord.

During the housing crisis, many homeowners who couldn't sell because they were underwater on their mortgages became landlords out of necessity. These were people like Alex Caffarini. In the aftermath of the financial crisis, the then-thirtysomething was ready to move on from his Schaumburg, Ill., condo.

He was offered a job to work for a consulting firm almost 700 miles away in Carlisle, Pa. The catch: Caffarini was still underwater on his mortgage, and he was unwilling to lose money on a short sale.

So Caffarini rented his place out, covering most of the mortgage and taxes, and moved. With lower expenses in Carlisle, he could afford to make extra mortgage payments to improve his equity. He eventually returned home to Schaumburg—Money's 9th Best Place to Live—but under much better financial circumstances.

Caffarini became a landlord during difficult economic times. Yet this strategy remains relevant in today's healthier economy, even after the market has been rebounding.

Turn your current home into the best place to live.

In 2011, Avik Chopra and his family bought a three-bedroom home in Milburn, N.J. Today it's worth $250,000 more than what they paid. But that's not money in the bank.

"It feels good to see the value rise, but we're still stuck in a home we've out grown," says Chopra, who has two young children. "All the other houses in our area have gone up too." But with more value comes more equity, which means Chopra has options. He's planning to borrow from his home to finance a second-floor addition.

If you're far along in paying off your mortgage, staying put can be wiser than taking on a new loan, especially if your mortgage is below the current 3.9% average for a 30-year fixed-rate loan.